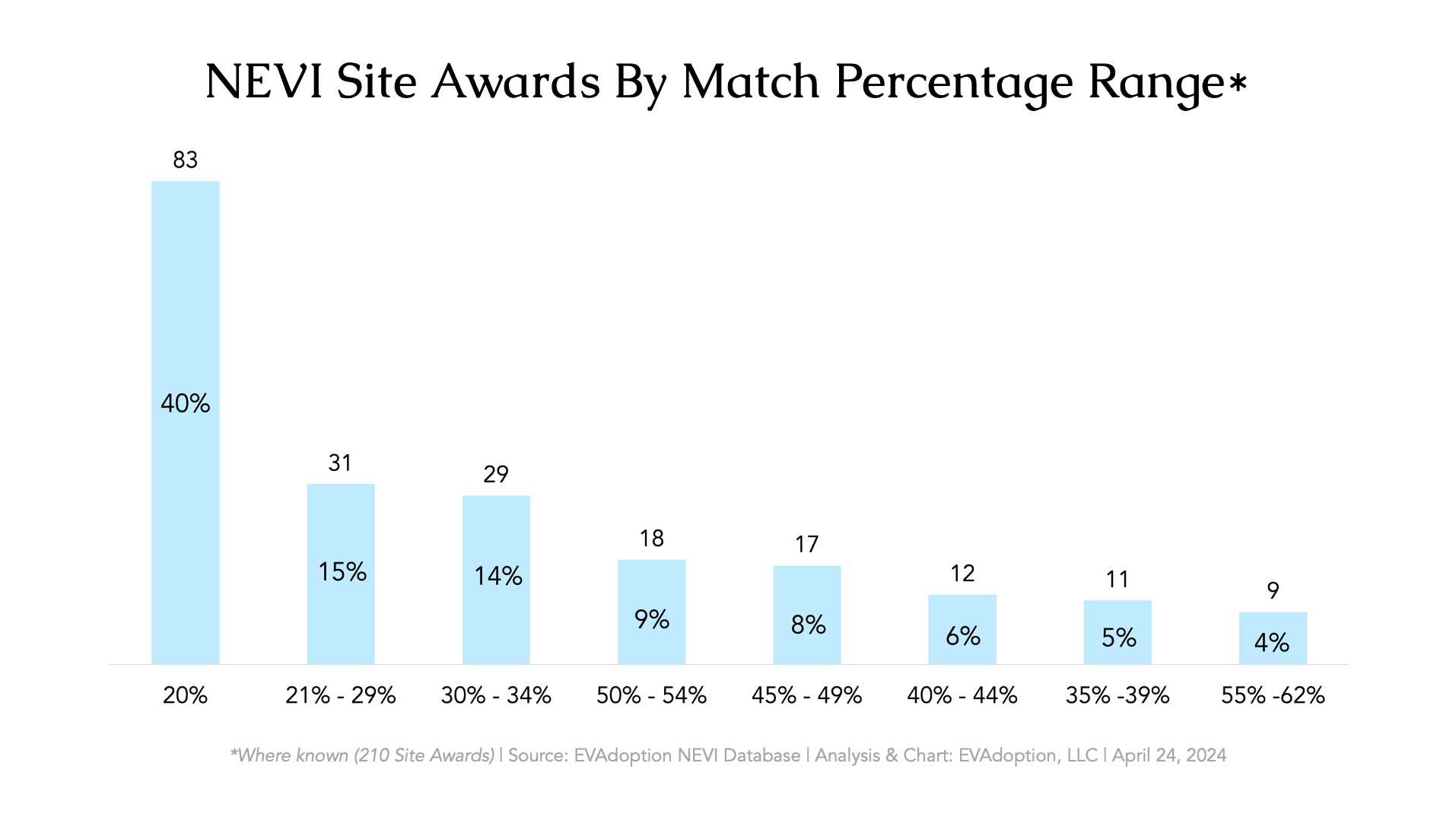

NEVI Site Awards By Match Percentage Range

Out of 210 winning NEVI applications (the amount for which we have obtained the match percentage amount), 40% of applicants have submitted a bid with the NEVI minimum 20% match.

Out of 210 winning NEVI applications (the amount for which we have obtained the match percentage amount), 40% of applicants have submitted a bid with the NEVI minimum 20% match.

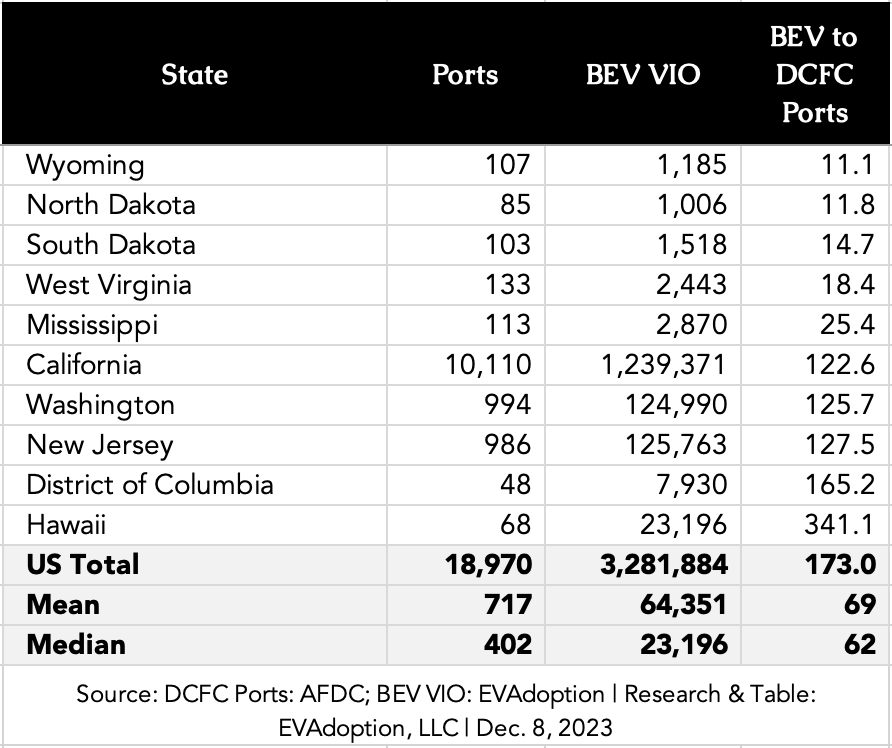

The “best” (lowest) ratio are rural and lower median-income states that have very low levels of EV adoption. In these states, the number of deployed DC fast chargers has simply outpaced BEV sales. DCFCs have been deployed, often from available grant programs and networks wanting to have at least a minimum presence in the state. But with BEV sales being so tiny, it makes the ratio look good.

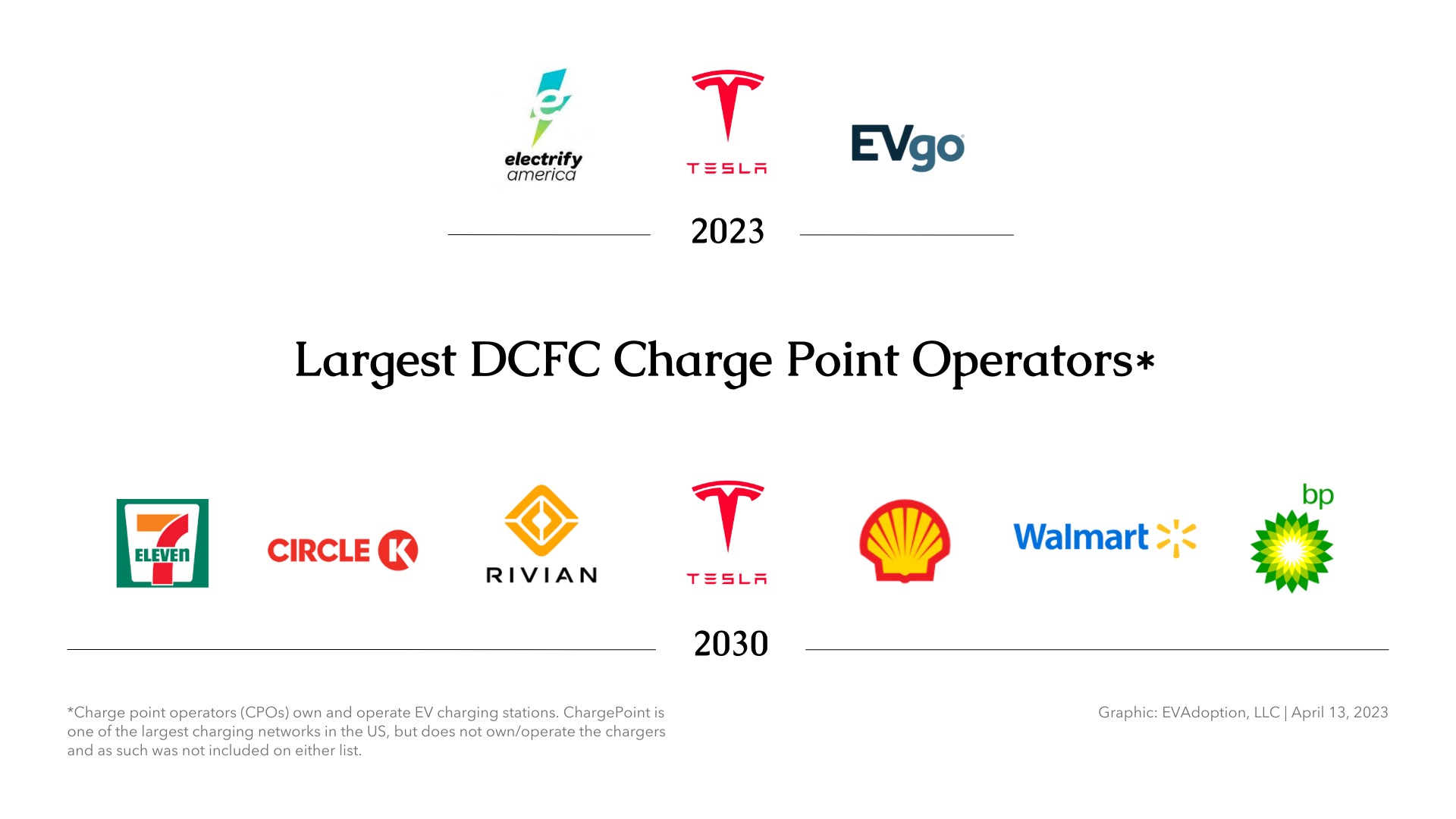

The largest US charge-point operators in 2030 are likely to be convenience store chains, travel center operators, retailers who already sell gasoline, and of course fuel retailers (gas station/convenience store companies).

Walmart announced that by 2030 it intends to build its own DC fast-charging network at “thousands of Walmart and Sam’s Club locations coast-to-coast.” This move by the world’s largest retailer has the potential to shakeup the fast charging industry.

There are 197 vehicles to every gas pump nozzle. If you drive an EV, there are 25.7 EVs to each public Level 2 + DCFC port and 1.6 to 1 if you include those chargers at home where you park your car each night.

Many electric vehicles have neck-slapping acceleration, exhilarating for drivers but a potential danger to others. OEMs should be focused on the charging experience — not 0-60 time.

$73/Month Through the National Electric Vehicle Infrastructure (NEVI) program, the US will be allocating $5 billion over 5 years to all 50 states (plus District

An estimated 27 million households living in single-family homes in the US cannot pull into their garage and plug in and charge an electric vehicle. Instead they will have to run the charging cable or extension cord (not advised) from inside the garage, install a charger outside the garage, somehow charge from the street, rely on public charging, or utilize a mobile charging service (charging as a service).

A new study on the reliability of DC fast chargers in the San Francisco Bay Area provides some much needed data and independent analysis to help hold EV charging networks accountable to a higher level of charging customer experience.

Beyond the use of confusing, technical and jargony terms and acronyms, a foundational communications problem with EV charging is that the industry doesn’t even agree on what the most basic of terms — EV “charging station” — actually refers to.

Out of 210 winning NEVI applications (the amount for which we have obtained the match percentage amount), 40% of applicants have submitted a bid with the NEVI minimum 20% match.

The “best” (lowest) ratio are rural and lower median-income states that have very low levels of EV adoption. In these states, the number of deployed DC fast chargers has simply outpaced BEV sales. DCFCs have been deployed, often from available grant programs and networks wanting to have at least a minimum presence in the state. But with BEV sales being so tiny, it makes the ratio look good.

The largest US charge-point operators in 2030 are likely to be convenience store chains, travel center operators, retailers who already sell gasoline, and of course fuel retailers (gas station/convenience store companies).

Walmart announced that by 2030 it intends to build its own DC fast-charging network at “thousands of Walmart and Sam’s Club locations coast-to-coast.” This move by the world’s largest retailer has the potential to shakeup the fast charging industry.

There are 197 vehicles to every gas pump nozzle. If you drive an EV, there are 25.7 EVs to each public Level 2 + DCFC port and 1.6 to 1 if you include those chargers at home where you park your car each night.

Many electric vehicles have neck-slapping acceleration, exhilarating for drivers but a potential danger to others. OEMs should be focused on the charging experience — not 0-60 time.

$73/Month Through the National Electric Vehicle Infrastructure (NEVI) program, the US will be allocating $5 billion over 5 years to all 50 states (plus District

An estimated 27 million households living in single-family homes in the US cannot pull into their garage and plug in and charge an electric vehicle. Instead they will have to run the charging cable or extension cord (not advised) from inside the garage, install a charger outside the garage, somehow charge from the street, rely on public charging, or utilize a mobile charging service (charging as a service).

A new study on the reliability of DC fast chargers in the San Francisco Bay Area provides some much needed data and independent analysis to help hold EV charging networks accountable to a higher level of charging customer experience.

Beyond the use of confusing, technical and jargony terms and acronyms, a foundational communications problem with EV charging is that the industry doesn’t even agree on what the most basic of terms — EV “charging station” — actually refers to.