Battery electric and plug-in hybrid vehicles purchased in or after 2010 may be eligible for the US federal income tax credit of up to $7,500. The credit amount varies based on the capacity of the battery used to power the vehicle. All current Tesla models and GM EVs do not qualify for the credit as each company surpassed the manufacturer 200,000 EV sales cap.

In 2022 we expect both Toyota and Ford to reach the 200,000 cap, followed by Nissan in 2023.

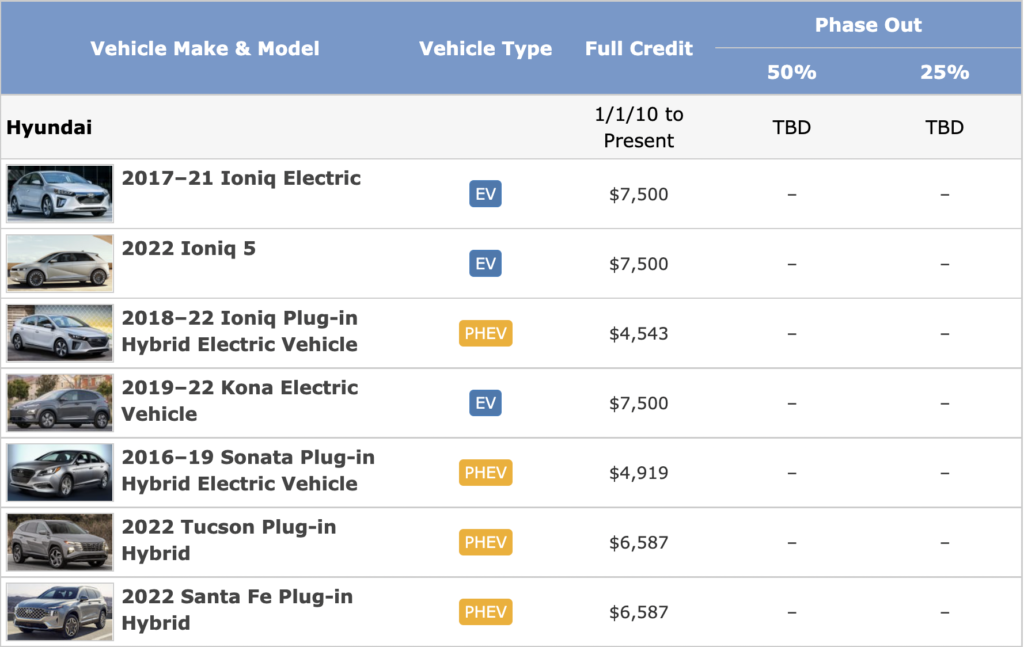

See how the IRS calculates the available tax credit for each EV model.

The federal tax credit is phased out over time beginning the second quarter AFTER the quarter in which a manufacturer reaches a total of 200,000 BEV or PHEV vehicles sold since 2010. Here is how the phase out works:

- The full amount of the EV qualifying tax credit is in place DURING the entire calendar quarter in which 200,000 EVs are sold by a manufacturer, AND through the subsequent quarter.

- Then the tax credit amount is reduced by 50% for the next 2 quarters.

- The credit is reduced again to 25% of the original amount for the subsequent 2 quarters.

- At that point the credit expires completely.